Is CD Laddering A Good Idea?

8/25/2025

When it comes to saving, most people want two things above all else: to keep their money safe and to see it grow. A CD ladder is one of the easiest ways to do both. By dividing your savings into several CDs with different maturity dates, you’re able to earn dependable returns while still having cash become available at different times instead of all at once.

So how does that actually work? And is it worth doing? Here we’ll cover what CD laddering is, how it plays out in real life, and why many people find it a smart way to reach their savings goals.

And if you already know you want to get started, you don’t have to wait. Open a certificate of deposit with Arkansas Federal Credit Union and start building your CD ladder today.

What Is A CD?

A certificate of deposit (CD) is a safe way to grow your savings. You deposit money for a set term, and in return, the bank or credit union pays a fixed interest rate. At Arkansas Federal, interest is credited monthly, so you earn along the way. When the CD reaches its maturity date, you can withdraw your principal and the interest you’ve earned or renew. Terms often range from 6 months to 5 years or longer. In exchange for your deposit commitment, CDs typically offer higher rates than a standard savings account.

What Is A CD Ladder?

Instead of placing all your money into just one CD, a CD ladder lets you divide it among several CDs with different end dates. Some finish sooner, giving you access to cash along the way, while others run longer.

This approach gives you regular access to your funds while also helping you take advantage of higher long-term CD rates.

If you want learn more about how to grow your savings using this method, check out our article on how to grow your savings smarter with CD laddering.

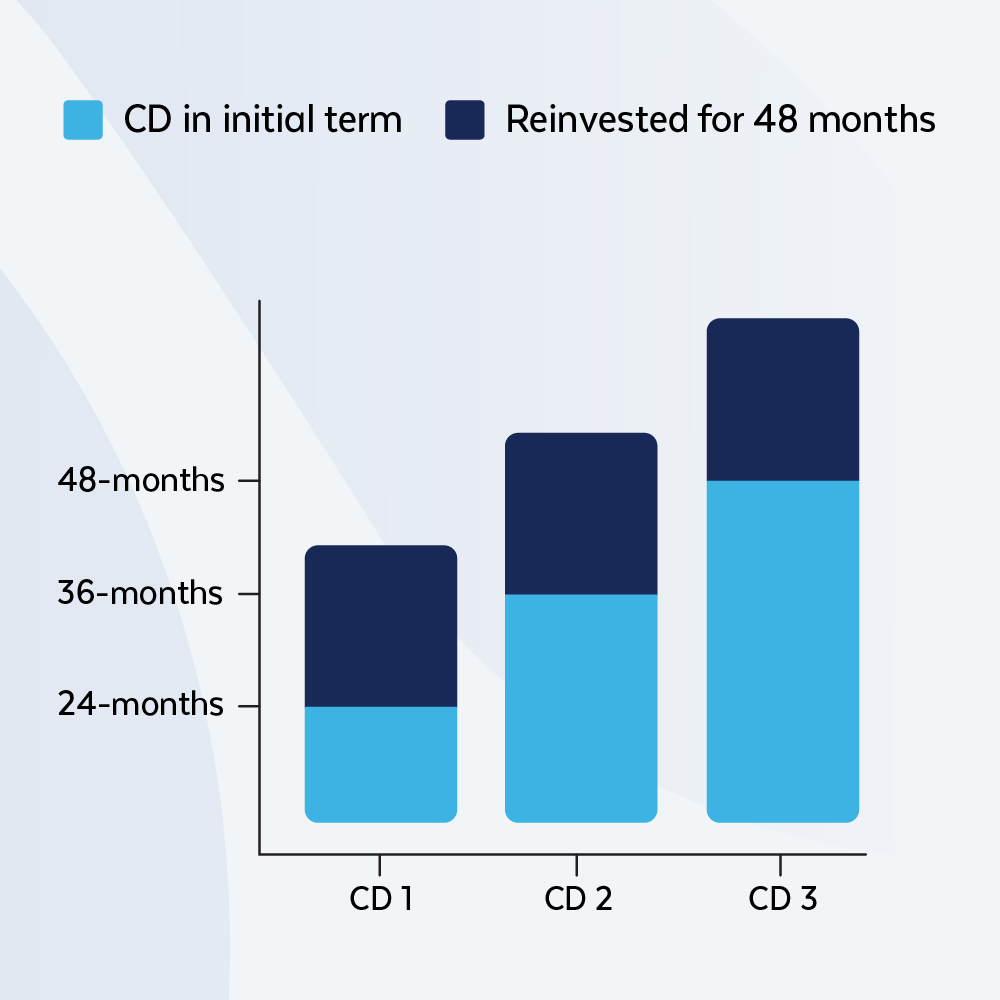

This chart shows how a certificate ladder can grow when you reinvest each maturing CD into a term. In this example, CDs start at 24, 36, and 48 months. As each matures, it’s rolled into another 48‑month certificate, building higher earning potential and staggered access to savings. This is just one example; you can build your ladder your way.

Benefits Of Having A CD Ladder

CD laddering offers a number of advantages, such as:

- Cash when you need it. Because each CD matures on its own schedule, a portion of your money will come back to you at regular intervals. That means you won’t have to worry about paying a penalty just to get to your savings.

- Locked-in earnings. Once you open a CD, your rate stays the same until it matures. No surprises, and no guessing—just steady, predictable growth you can plan around.

- Growth with flexibility. A ladder lets part of your money take advantage of higher long-term rates, while the rest is available sooner if you need it.

- Room to adjust. When one CD matures, you can reinvest at the current rates. If rates rise, you’ll benefit, and if they fall, the CDs you already locked in will keep earning at the higher levels.

- Built-in protection. Because CDs are federally insured (NCUA insured at credit unions and FDIC insured at banks), your money is protected while it grows.

Things To Consider With CD Laddering

While CD ladders are a strong strategy for many savers, it helps to keep a few considerations in mind so you can decide how this approach fits your goals.

- Access before maturity. If you need your money early, most CDs charge a penalty for withdrawing before the maturity date. A ladder helps lessen that risk since part of your money becomes available regularly, but it’s still something to keep in mind.

- Keeping track. Each CD in your ladder has its own timeline. It’s important to note those maturity dates so you’ll know when it’s time to reinvest or use the funds.

- Rates may change. When a CD matures, the new rates available might be higher or lower than before. This can affect how much you’ll earn going forward.

- Inflation impact. CDs are safe and predictable, but sometimes inflation can grow faster than your returns. Many people are comfortable with that tradeoff because of the stability CDs provide.

- How much to put in. Most CDs require a minimum deposit—often $1,000 or more. Beyond that, the more you spread across different terms, the more flexibility and growth your ladder can provide.

Is CD Laddering Right For You?

CD laddering can be a smart fit if you’re looking for a balance of safety, growth, and access. It often appeals to people who want their savings to grow without taking on extra risk, but also don’t want all their money tied up in one place for years at a time.

It’s especially worth considering if you:

- Value the stability of guaranteed returns.

- Like knowing that part of your money will come back to you at set intervals.

- Prefer something that helps reduce the chance of being locked into one single rate for too long.

So, Is CD Laddering A Good Idea?

For many, yes. A CD ladder gives your savings a chance to grow while still letting you tap into cash at different points along the way. By dividing your money into CDs with different terms, you avoid having everything locked up for years at a time, yet you still get the benefit of longer-term rates.

This mix of growth, access, and protection makes CD laddering a practical option for savers who want steady progress without taking on extra risk.

Alternatives To CD Laddering

A CD ladder is a great savings strategy, but it’s not your only choice. Depending on your goals, you might also look at:

- High-Yield Checking Accounts. These accounts give you the best of both worlds: everyday access to your money plus a higher return than a standard checking account. At Arkansas Federal, our Elite or Premium checking accounts are popular choices for members who want to use their money freely while still earning a great rate.

- Money Market Accounts. A money market is a good choice if you want your savings to grow without locking into a term. You can transfer or access your money whenever you need to, as often as you like, while still earning a competitive rate. The return may not be as high as a CD, but it’s usually better than a standard savings account.

CD Ladder Examples

Let’s say you have $50,000 to invest. There are different ways to build a CD ladder, but here are two common approaches.

Example 1: Even split

In this setup, the money is divided evenly across several CDs with terms that range from 6 months to 5 years. As each one reaches its maturity date, another becomes available. That means you get steady access to cash while the rest of your savings continues to earn interest.

Example 2: Custom mix

If you want more flexibility at the beginning, you can place smaller amounts into the shorter terms and larger amounts into the longer ones. This way, you’ll have some money available sooner while the bigger portions are set aside to take advantage of the higher long-term rates.

There isn’t just one way to build a CD ladder. Some people divide their money evenly across several terms, while others put more into the longer CDs and less into the shorter ones. It really comes down to how much access you want to your money and how patient you’re willing to be for higher returns.

These examples are only meant to give you an idea of how a ladder can work. In practice, you can arrange one in many different ways, and the setup should reflect how you like to manage your savings.

Curious to see how much you could earn? Take a look at our current rates and use the calculator to explore your potential earnings.

Open A Certificate Of Deposit With Arkansas Federal Today

A CD ladder can help you grow your savings while keeping it protected. You’ll earn a set return, have access to part of your funds at regular points, and know your deposits are federally insured.

Start your CD ladder strategy today. Open a certificate of deposit with Arkansas Federal and enjoy guaranteed growth, dependable returns, and complete financial confidence. Visit us online or at your local branch to learn more.